People borrow money for many reasons. Sometimes it’s an emergency or a big purchase they can’t cover in cash. But often, the story runs deeper than numbers. Borrowing is not just a financial act—it’s a psychological one. The decision to take a loan can be influenced by emotions, cultural habits, peer pressure, and even marketing strategies that play directly on our desires. Understanding these motives helps us use credit wisely and avoid the traps that lead to debt stress and constant calls from collection agencies.

Emotional Triggers Behind Borrowing

When we think about loans, we imagine rational choices: a family financing a house, a student covering tuition, or a small business expanding operations. Yet many people borrow even when they don’t strictly need to. Emotional triggers like fear of missing out, the desire for status, or stress relief play a huge role. For instance, buying the latest smartphone on credit may feel like a necessity in a social circle where appearances matter. This creates a loop where borrowing becomes less about solving real problems and more about satisfying temporary emotions.

The Social Side of Credit

Credit is not only about money—it’s about belonging. People often take loans because “everyone does it.” In societies where credit cards are part of daily life, avoiding them might even feel unusual. Peer influence pushes individuals into debt because refusing can seem like rejecting modern life itself. This is particularly visible in younger generations, where social media amplifies lifestyle competition. Seeing friends travel, buy cars, or wear designer clothes can make borrowing feel like the only way to keep up.

Habits That Turn Into Debt

Another layer of borrowing psychology lies in habits. Once someone starts using credit to cover small expenses, it can quickly snowball. The brain adapts to the idea of “future money” being available, creating a comfort zone where debt feels normal. This can be dangerous. What begins as an occasional convenience becomes a long-term pattern, with interest rates piling up. Breaking free requires self-awareness and a conscious effort to reframe credit as a tool, not a lifestyle.

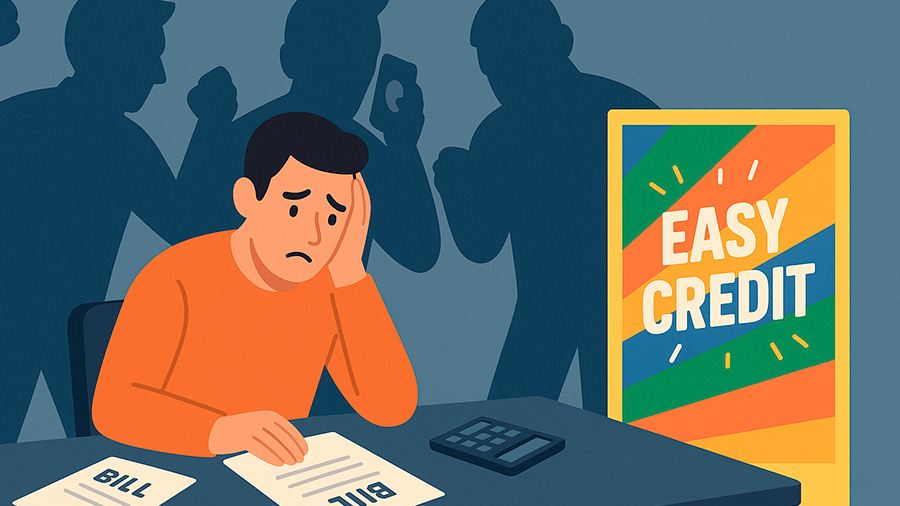

Marketing and the Illusion of Necessity

Banks, lenders, and fintech companies know how human psychology works. They design ads that highlight the convenience of borrowing, making loans seem like smart opportunities instead of financial obligations. “Buy now, pay later” slogans reduce the perception of risk, while rewards programs tied to credit cards make borrowing feel rewarding. This illusion of necessity tricks people into believing that not taking a loan means missing out on benefits, even when the expense itself is optional.

The Role of Stress and Crisis

Stress and uncertainty push many toward credit. Unexpected medical bills, job loss, or inflationary pressures can force households into borrowing cycles. But psychology also plays a part. In moments of crisis, the brain seeks quick relief. Borrowing offers instant peace of mind, even if it creates long-term burdens. This explains why some families take loans with unfavorable conditions—they prioritize short-term survival over future consequences.

When Borrowing Becomes Compulsive

In some cases, borrowing becomes a compulsion. Similar to gambling or shopping addiction, credit dependency grows from psychological needs like control, escape, or validation. People in this situation often borrow for reasons unrelated to actual necessity, leading to spirals of debt. Recognizing the difference between functional borrowing and compulsive borrowing is essential to prevent financial collapse.

Common Psychological Reasons for Taking Loans

- Fear of missing out on opportunities

- Peer pressure and social comparison

- Stress relief and emotional comfort

- Advertising influence and perceived rewards

- Habitual reliance on credit

Practical Ways to Resist Unnecessary Borrowing

The good news is that people can take control of their borrowing habits by addressing the psychological side of debt. Strategies like building emergency savings, practicing mindful spending, and setting personal rules for credit use can reduce unnecessary borrowing. Financial education also plays a key role—understanding how interest accumulates makes the cost of impulsive loans harder to ignore.

Tips for Smarter Borrowing

- Pause before taking any loan—ask if the expense is a true necessity.

- Compare the long-term cost of borrowing versus saving.

- Limit exposure to ads that encourage “easy money.”

- Track expenses to spot habits that fuel credit dependence.

- Consider alternatives like community support or side income before borrowing.

The Cycle of Borrowing: A Table of Motives

To better understand why people borrow when they don’t need to, here’s a breakdown of psychological factors that drive borrowing behavior:

| Psychological Trigger | How It Works | Result |

|---|---|---|

| Fear of Missing Out | Belief that opportunities or status will be lost without spending | Borrowing for non-essential purchases |

| Stress Relief | Using borrowing as a quick solution to emotional pressure | Debt increases, relief is temporary |

| Peer Pressure | Desire to match friends’ lifestyles | Loans for unnecessary luxuries |

| Marketing Influence | “Buy now, pay later” messages reduce risk perception | Unplanned debt grows |

| Habit | Regular use of credit feels natural | Chronic reliance on loans |

Debt Collection and Psychological Pressure

When borrowing goes too far, the consequences shift from psychological to practical. Debt collectors and agencies enter the picture, applying pressure that creates even more stress. The cycle continues: people who once borrowed to escape stress now face daily anxiety from repayment demands. Some even start searching for resources like 9784445700 call explanation to better understand collection practices. This highlights the full circle of borrowing psychology—what starts as emotional relief can end in emotional distress.

A Balanced View on Borrowing

Not all borrowing is bad. Loans can provide access to education, homes, and opportunities that truly improve life. The key difference lies in awareness. Borrowing with purpose, clear repayment plans, and realistic limits keeps debt under control. Borrowing without reflection, driven by emotions and habits, turns helpful tools into chains that weigh down financial freedom.

Conclusion: Mastering the Mind Before Money

The psychology of borrowing explains why people often take loans they don’t really need. From fear of missing out to social competition and emotional relief, credit decisions are rarely as rational as they appear. Recognizing these triggers is the first step toward change. By mastering the mind before managing money, people of all ages can use loans as tools rather than traps. Borrowing doesn’t have to mean endless calls from collectors—it can mean opportunity, if handled with awareness and discipline.